( Disponible en anglais seulement )

Draft legislation making significant changes to the foreign affiliate provisions of the Income Tax Act (Canada) (the “Act”) was released by the Department of Finance on August 19, 2011.

The new provisions deal with upstream loans from and other indebtedness owing to foreign affiliates, a new hybrid surplus account related to certain capital gains, foreign affiliate reorganizations, changes to the surplus distribution ordering rules, capital losses of foreign affiliates and stop-loss rules.

This article addresses only the new rules applicable to so-called “upstream loans”.

Prior to these changes, it was possible for a foreign affiliate with taxable surplus to make a loan to a Canadian resident corporate shareholder or a related Canadian resident corporation, instead of paying dividends, without adverse Canadian tax consequences. Loans could be an attractive alternative to dividends because a dividend from a foreign affiliate out of taxable surplus must be included in income and may not be completely offset by a deduction under subsection 113(1) of the Act in respect of underlying foreign taxes (if any) paid by the foreign affiliate. A loan may also have been preferred if dividends were not possible under foreign law or would be subject to an uneconomic level of withholding tax in the foreign jurisdiction. There were no rules requiring a loan from a foreign affiliate to be included in income if not repaid within a certain period of time. The primary target of the new rules regarding loans from and other indebtedness to foreign affiliates appears to be these “upstream loans”, however, the scope of the new rules is actually much broader.

The new upstream loan rules apply where a Canadian resident, any other person with whom the Canadian resident does not deal at arm’s length (other than controlled foreign affiliates within the meaning of section 17 of the Act) or certain partnerships is indebted to a foreign affiliate (“FAco”) of the Canadian resident. If the loan of other indebtedness is not repaid within two years after it arose, then, subject to certain exceptions described below, each Canadian resident taxpayer for whom FAco is a foreign affiliate must include a portion of the loan or other indebtedness in its income based on the taxpayer’s surplus entitlement percentage.

The income inclusion can be avoided if the loan or other indebtedness is fully repaid within two years after it arose (but the repayment cannot be part of a series of loans and repayments). For loan or other indebtedness owing to a foreign affiliate before August 19, 2011, the two year period for repayment commences on August 19, 2011. In other words, the loan or other indebtedness must be repaid on or before August 18, 2013 to avoid the application of the new rule.

Certain exceptions apply where the loan or other indebtedness arose in the ordinary course of the foreign affiliate’s business or is a loan made in the ordinary course of the foreign affiliate’s money lending business where bona fide arrangements were made at the time the indebtedness or loan arose for repayment within a reasonable time.

A striking feature of the new upstream loan rules is that a Canadian resident can be required to include an amount in its income even if the Canadian resident is not the person indebted to FAco. Where any person with whom a Canadian resident does not deal at arm’s length (except controlled foreign affiliates within the meaning of section 17 of the Act) becomes indebted to a foreign affiliate of the Canadian resident, then (subject to the ordinary course exception described above) the Canadian resident can have an income inclusion. Indebtedness of certain partnerships to the foreign affiliate can also trigger an income inclusion.

A Canadian resident can be required to include an amount in its income under the new upstream loan rules, even where the Canadian resident does not directly or indirectly benefit from the loan or other transaction giving rise to the indebtedness. This is illustrated in the following examples (which both assume the ordinary course exception does not apply).

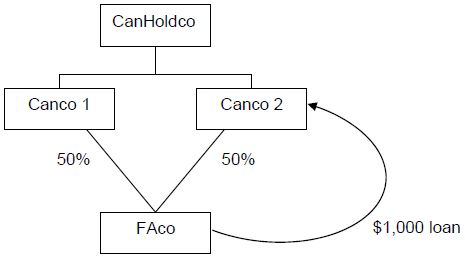

See diagram 1.

{kind=link}

The $1,000 loan to Canco 2 will require each of Canco1 and Canco 2 to include $500 in income unless the loan is repaid within two years (other than as part of a series of loans and repayments).

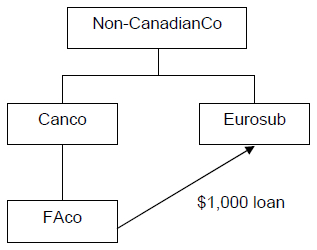

See diagram 2.

{kind=link}

The $1,000 loan to Eurosub will require Canco to include $1,000 in income unless the loan is repaid within two years (other than as part of a series of loans and repayments).

If a Canadian resident individual becomes indebted to a foreign affiliate and the loan or other indebtedness is not repaid within one year after the end of the taxation year of the foreign affiliate, subsection 15(2) of the Act will generally require the amount of the loan or other indebtedness to be included in the individual’s income. The new upstream loan rules do not apply where subsection 15(2) applies and will therefore generally be more significant for corporations than for individuals. However, the upstream loan rules could apply to a Canadian resident individual in circumstances where subsection 15(2) would not. This is illustrated in the following example (which assumes the ordinary course exception does not apply).

See diagram 3.

{kind=link}

The $1,000 loan to Canco will require Mr. X to include $500 in his income unless the loan is repaid within two years (other than as part of a series of loans and repayments).

The above examples show the broad scope of these new rules. The broad scope makes the “upstream loan” label given to these new rules by the Department of Finance dangerously misleading. It is not only loans that can give rise to mandatory income inclusions. Other indebtedness, e.g., unpaid purchase price, can have the same result. Also, transactions giving rise to indebtedness to a foreign affiliate which are not obviously “upstream” can trigger an income inclusion. A careful review of any loan or other indebtedness owing to a foreign affiliate of a Canadian resident taxpayer should be undertaken to identify situations that could result in income inclusions under the new rules.

If the loan owing or other indebtedness to the foreign affiliate is repaid after the two year period and a Canadian resident taxpayer had to include an amount in income in respect of the indebtedness, then the taxpayer is entitled to a deduction in the year of repayment. Where the loan or other indebtedness is only partially repaid, the deduction is prorated accordingly.

Where a Canadian resident taxpayer has an income inclusion as a result of a loan from or other indebtedness to a foreign affiliate, the taxpayer may claim a deduction under proposed subsection 90(6) of the Act for the portion of that amount that it could have received as an actual dividend without Canadian tax by reason of deductions claimed for exempt surplus, hybrid surplus and hybrid underlying tax (“HUT”) or underlying foreign tax in respect of taxable surplus of the foreign affiliate.

The deduction based on exempt surplus is only available if there is sufficient exempt surplus to cover a hypothetical dividend in an amount equal to the deduction claimed under proposed subsection 90(6) of the Act.

The deduction based on hybrid surplus is only available if there is sufficient hybrid surplus and HUT and if the foreign tax on the capital gains giving rise to hybrid surplus is at least equal to the Canadian tax rate applicable to capital gains realized by a corporation.

The deduction based on underlying foreign tax (“UFT”) related to taxable surplus is generally only available if the foreign affiliate has sufficient UFT such that the grossed-up UFT that could be designated in respect of a dividend out of taxable surplus is at least equal to the deduction claimed under proposed subsection 90(6).

These deductions based on hypothetical dividends are only available if no dividends are paid to the taxpayer or any other Canadian resident with whom the taxpayer does not deal at arm’s length by any foreign affiliate whose surplus accounts are relevant to the deductions claimed. At the Canadian Tax Foundation’s recent 2011 annual conference, a Department of Finance representative indicated that some relieving modifications are being considered regarding the restriction on payment of dividends while the loan or other indebtedness is outstanding.

The deductions based on hypothetical dividends are only available if the relevant surplus accounts have not been relied upon to support a deduction in respect of any loan or other indebtedness. The amount of the hypothetical dividend deduction must be included in income in the next year. The taxpayer may then claim a hypothetical dividend deduction in that next year based on the surplus accounts in the next year.

The draft legislation leaves some uncertainty as to which surplus accounts can be relied upon for the hypothetical dividend deduction. Clearly, the surplus accounts of the foreign affiliate to whom the loan or other indebtedness is owed are included. Clarification is desirable on whether the surplus accounts of subsidiaries of that foreign affiliate should also be included. It has been suggested that a Canadian resident taxpayer should be able to offset previously taxed FAPI from the relevant foreign affiliate against the income inclusion for loan or other indebtedness owing to that foreign affiliate. The Department of Finance appears to be sympathetic to these situations and suggestions.

It is likely that there will be changes to the proposed legislation before it is enacted to respond to submissions and to correct unintended consequences. Stay tuned.